The CARES Act and You: What You Need to Know Now

Submitted by Bernhardt Wealth Management on April 2nd, 2020In response to the worldwide crisis created by the COVID-19 pandemic, last week President Trump signed the largest relief package in history: the Coronavirus Aid, Recovery, and Economic Security (CARES) Act. The vast majority of Americans will benefit directly from the $2 trillion in aid included with this bill, which includes a direct payment to most taxpayers and their families. Here’s what you need to know about how much you’ll receive in your stimulus check and how to make sure you get it.

Who gets a check? About 94% of American taxpayers are eligible to receive a stimulus check from the federal government. These are the criteria you must meet:

- Be a U.S. citizen or legal resident

- Have a work-eligible Social Security number

- Not be a dependent or eligible to be a dependent of any other taxpayer

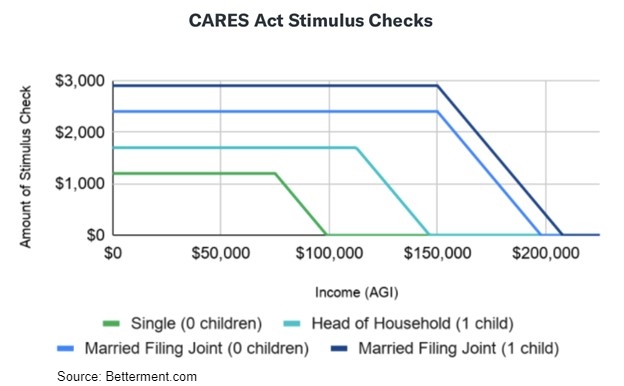

How much will my check be? Checks to eligible individuals will be $1,200 or less, depending on your adjusted gross income (AGI) as reported on your tax return for either 2018 or 2019. Couples filing joint returns will be eligible to receive $1,200 each, for a total of $2,400. Families with children age 17 or younger will receive $500 for each child.

- If you are a single filer with AGI of $75,000 or less, you will receive $1,200.

- If you are married filing jointly with AGI of $150,000 or less, you will both receive $1,200.

- If you are single, head of household with AGI of $112,500 or less, you will receive $1,200.

- The amount of your check will decrease by $5 for every $100 by which your AGI exceeds the threshold for your tax filing status.

The following chart will help you estimate the size of your check, based on your AGI. To see your calculation, find the colored bar that matches the tax filing status on your most recently filed return.

If you think that your check would be bigger based on your filing status in 2018, you may wish to delay filing your 2019 return until after you’ve received your check. Remember, for 2020, you do not have to file your return until July 15.

How do I get my check? As long as you filed a tax return in 2018 or 2019, you probably don’t have to do anything. The IRS will send the payments via direct deposit or on a paper check if you are not set up on direct deposit (the checks will be mailed to the address shown on your tax return). If you haven’t filed a tax return in either 2018 or 2019, you will need to file at least a simplified return for 2019 in order to qualify for a check. The IRS has information on free assistance with filing your return here: Free Tax Return Preparation.

When will my check arrive? The CARES Act stipulates that the IRS must process the checks as fast as possible. Checks will probably start going out in about two or three weeks.

What should I do with the money? These direct payments are intended to provide direct assistance to American taxpayers who have lost wages, jobs, or opportunities because of COVID-19. Priorities for the best ways to use your stimulus check include:

- Paying for necessities (food, shelter, transportation, medicine)

- Making minimum payments on credit cards or other debt. Staying current will prevent having to dig out of a deeper hole when life returns to normal.

- Paying off high-interest debt if possible. The less debt you carry, the more flexible you can be in good times and bad.

- Starting or adding to your emergency fund. You should try to keep six months’ worth of expenses in your emergency fund.

- Saving for retirement. If you have extra money left over, consider opening or adding to an IRA or other retirement plan.

- Helping others in need. If your employment has been less affected by the pandemic, you may wish to allocate some or all of your stimulus check to a friend, family member, or neighbor who needs extra assistance.

We are going through a tough time in our country and all over the world right now. It’s more important than ever to stay informed, stay alert, and practice good public health habits. If we all do our part and help each other when we can, we’ll be stronger, better people as a result.

If you have questions about the stimulus package, your benefits, or any other financial matter, I suggest that you call your CPA, financial advisor or us. We would be happy to talk.